Did you know your credit score can cost you hundreds of thousands of dollars over the course of the mortgage?

If you are planning to purchase a home with a mortgage, you’ll want to make sure your credit scores are 740 and above to qualify for the best rates on jumbo loans and more loan options. According to NerdWallet, “for most loan types, the credit score needed to buy a house is at least 620.”

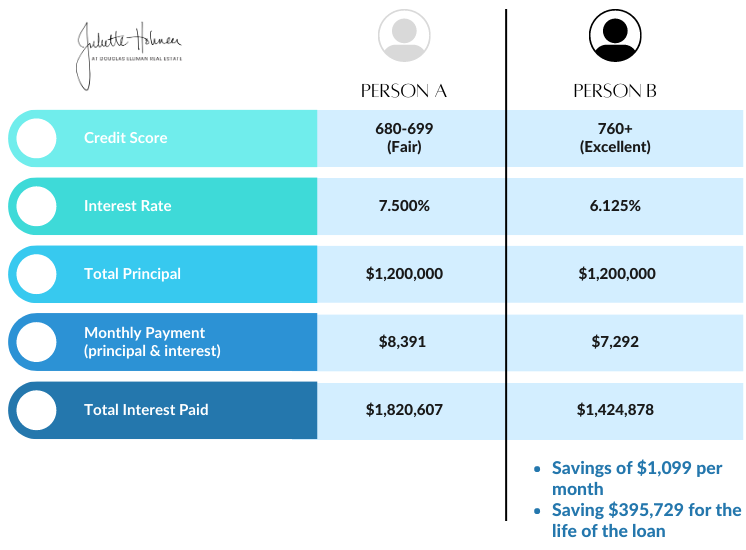

Example of Fair Credit vs. Good Credit

Let’s take a look at how having a higher credit score will save you money over the life of your loan.

Here is an example of a jumbo 30-year fixed loan on a$1,500,000 home purchase with 20% down payment.

*Using Nerdwallet.com Mortgage Calculators to find best interest rates as of 1.5.2023 based on credit score and paying minimum to none for lender fees.

Increasing your credit score by 61-80 points could save you $1100/ month or almost $400,000 over the life of your loan!

5 Factors that affect your credit score/ how to build better credit

- Pay your bills on time.Payment history is the biggest factor in calculating your credit score. It accounts for 35% of your FICO Score calculation (https://www.forbes.com/advisor/credit-score/rebuilding-credit-after-bankruptcy/).

- Credit utilization.Keep your credit balances low to less than 30% of the available credit you have. It’s great to use credit cards for their points and rewards, however, paying off the balances each month will significantly help your credit score as this makes up 30% of your FICO Score calculation (https://www.forbes.com/advisor/credit-score/rebuilding-credit-after-bankruptcy/).

- Credit age.Keep your credit cards open. Having longevity in your accounts in good standing helps show lenders you have more experience managing credit.

- Credit mix.Have different types of credit. Revolving accounts are your credit cards that can fluctuate month-to-month, while installment credit have a fixed end date for repayment such as mortgages, car loans, and student loans. However, don’t take out a new loan if you don’t need it!

- Recent credit.Applications you file for new credit cards, car loans, etc. can impact your credit with hard inquiries. These will fall off typically within 2 years, however, it is best to not apply for new lines of credit prior to qualifying for your mortgage.

Monitor your progress by checking your credit periodically. You an access a free copy of your credit report through AnnualCreditReport.com once per year. CreditKarma.com and Myfico.com are sites that can help monitor your report and see your credit scores. Most credit cards are now offering access to your credit report and/or score for free.

Once your credit score reaches at least 620 or hopefully 680+ then you will be more successful at securing better financing options for your home purchase.

Tips to keep your credit on track while applying for home loans and throughout the purchase of your home

- Pay credit card balances strategically. As mentioned above, you should be using less than 30% of your credit limit on any card. Pay down the balance before the billing cycle ends or pay several times throughout the month if it’s a card you use often. Then when the credit bureaus pull the balance, it will be low.

- Don’t open new lines of credit or credit cards while you are shopping for a new home. Avoid buying or leasing a new car, putting large ticket items (new washer/dryer, TV) on your credit cards, or opening new lines of credit. You want to minimize hard inquiries on your credit report (credit applications) at least 9-12 months before trying to get a mortgage.

- Ask for higher credit limits. Most credit cards make it easy to ask for an increase in your credit limit- online or maybe a phone call. If your income has gone up this is a good reason to ask. Then if your balance stays the same but the limit goes up you now have more room on that card which lowers your credit utilization.

If you have a low credit score or limited history, you should utilize the free credit report sites mentioned previously to understand where your score is at now and build on that. Remember, it takes time to build good credit. There may be a few ways you can lower your score fast, however, the best advice is to create consistent habits as outlined above and work with professionals to help guide you along the way to home ownership.